The 3 names that own UK's Free Streaming shelf

7 UK AVOD services, 1 month of data and 3 names that took 84% of it.

Free Streaming was supposed to tear down the gates. No subscription, no broadcast empire required, just content and an audience meeting on a shelf. Reach the viewers who have tired of paying for yet another subscription and do it without the decades of brand and infrastructure the old broadcasters spent generations building.

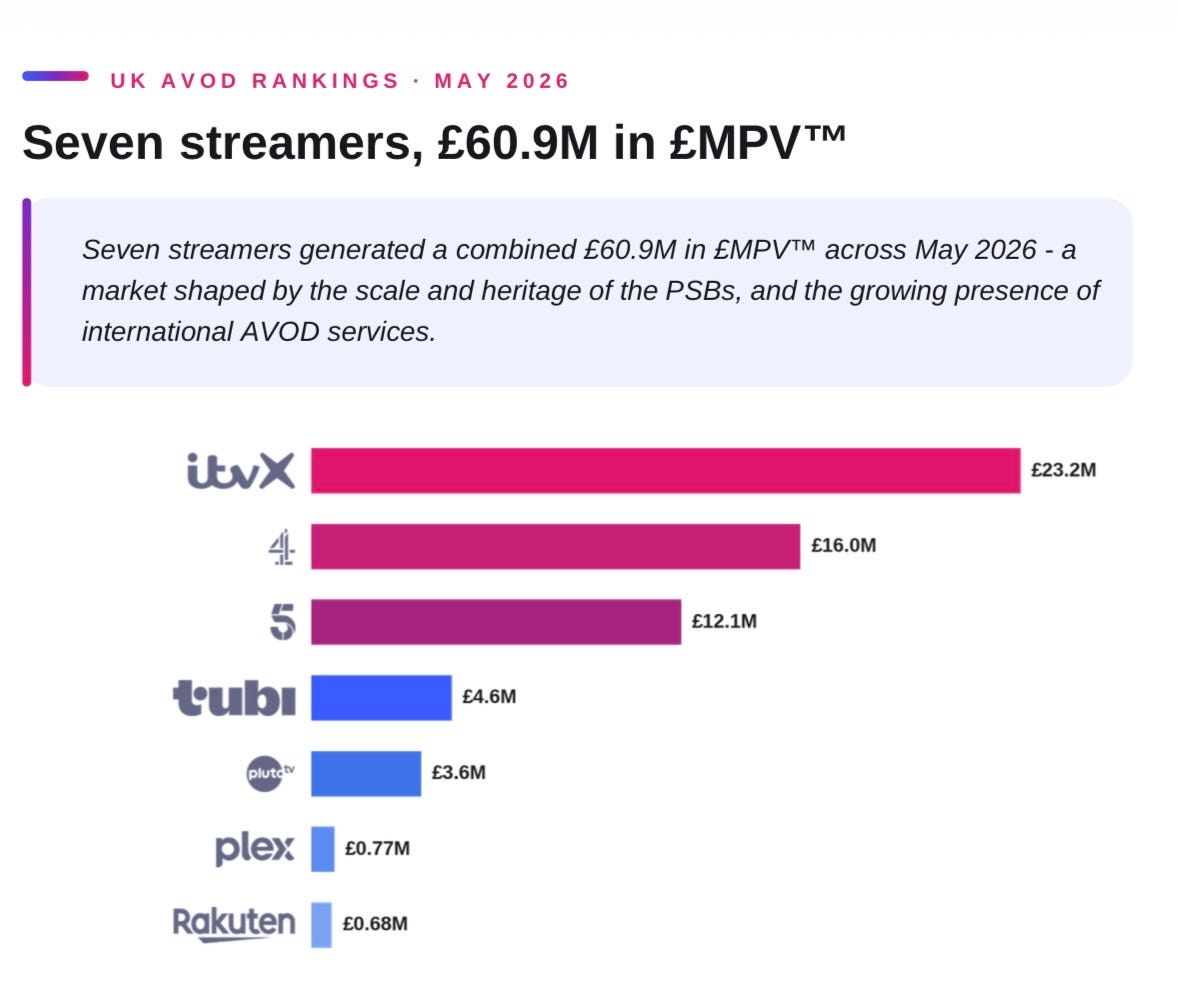

For our newest edition of Above the Fold with Looper Insights, we decided to test that pitch against hard placement data. We tracked 7 UK AVOD services across 14 streaming platforms, from Fire TV and Samsung to Sky Q and PlayStation consoles. Across May 2026, those 7 generated £60.4M in Media Placement Value (£MPV) over 29,785 promotional spots and 2,433 unique titles.

So who actually walked away with that £60.9M? Let’s find out.

Today at a glance:

The number that settles it

Why the broadcasters still win

What this means if you are not a PSB

Plus the full May rankings and placement data in our latest report.

The number that settles it

Three names took 84% of the market.

ITVX, Channel 4 and Channel 5 generated £51.2M of the £60.9M in £MPV across May. The four international streamers, Tubi, Pluto TV, Plex and Rakuten TV, split the remaining £9.7M between them. ITVX alone, at £23.2M, outweighs all four of those services combined by nearly two and a half times. One caveat: Rakuten TV runs both a free ad-supported service and a transactional store, so its figure reflects placement visibility across both rather than AVOD alone.

So the Free Streaming shelf that was meant to let new entrants reach audiences without a broadcast empire behind them spent May promoting, overwhelmingly, three broadcast empires.

Why the broadcasters still win

Scale explains most of it. ITVX ran the highest spot count of any service in the analysis and placed it across all 14 tracked platforms. Channel 4 matched that 14-platform spread, the joint widest in the market. When a service appears on every major device in UK homes and does so thousands of times over, the placement value compounds in a way a narrower footprint cannot reach.

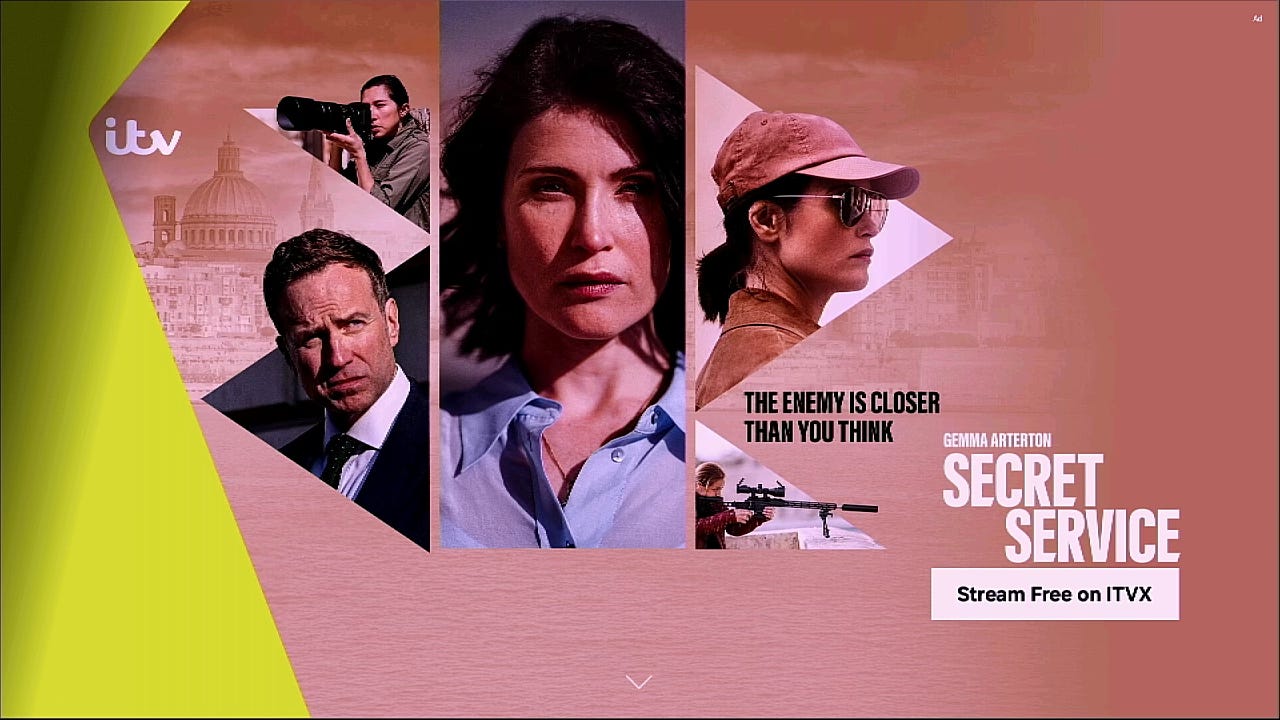

The content behind the spots tells the rest and each broadcaster promoted to a clear identity. ITVX led on drama, headed by the Gemma Arterton espionage thriller Secret Service, which topped the entire market for the month.

Channel 4 promoted to a different audience entirely, with returning reality franchises like Celebs Go Dating anchoring its slate.

Channel 5 built its month on homegrown drama, led by Number One Fan and its flagship commission The Hardacres.

What unites the three is not so much a shared content strategy but the machinery underneath. Amazing content, decades of platform relationships, the carriage deals, the prominence agreements and the budgets a broadcaster accumulates. That machinery is what the home screen “rewards”.

What this means if you are not a PSB

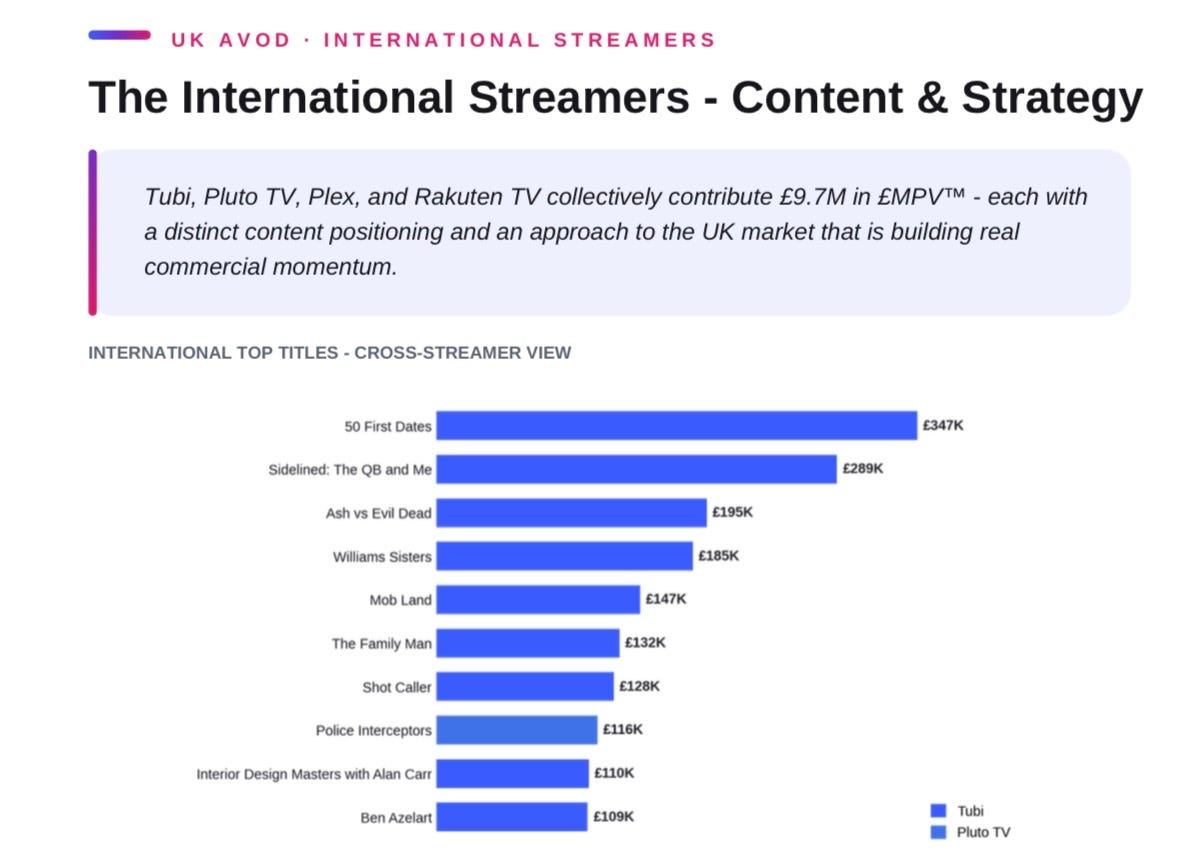

The international tier reached £9.7M in May, with Tubi and Pluto TV doing most of the lifting.

Tubi leads and it is doing something the others are not. Its slate leans on YouTube-native franchises like Ben Azelart, Jordan & Salish Matter and The Royalty Family, creator content with no equivalent at scale on any other UK AVOD service. Ampere Analysis put Tubi UK’s catalogue growing 99% across 2025, the fastest of any AVOD service it tracked. So the May prominence sits on a base still expanding fast.

Then the lesson for whoever owns the content rather than the platform it runs on. Police Interceptors ran on both Channel 5 and Pluto TV in May, promoted on two unrelated free services and counted on both. One hour of British factual telly, working twice in the same month. If you are a rights holder choosing between an exclusive and going wide, that is the argument for wide.

The other lesson is consistency. The broadcasters win on presence. They turn up on all 24 platforms, week after week and no single slot has to carry them. A challenger can match a PSB on one placement. Holding that across the whole market, through the quiet weeks and the loud ones, is what takes years to build.

None of this is a UK quirk. The home screen behaves the same way across European CTV and the question for every broadcaster and streamer is whether they are putting enough behind prominence to match their ambition.

This piece shows three broadcasters owning 84% of the shelf. The report shows you the placement-by-placement detail of how, every title's £MPV and the creative that earned it. Get it here.

That’s it for today. Comments, shares or likes come a long way 🙏🏻

Catch up on our previous reads: