Prime Video runs the shelf while HBO Max runs the show.

Home screen winners, invisible giants, local resilience and a $22 billion question for Amazon.

For our newest edition of Above the Fold with Looper Insights, we tracked home screen placement across 4 markets in March, covering 45 devices in total spanning the US, UK, Germany and Australia. One name sat at the top of the app visibility rankings in every single one of them: Prime Video. The streamer led the app chart across all four markets which reflects years of sustained investment in platform relationships, device integration and promotional discipline. Yet at the programme level, the titles filling those same home screens belonged almost entirely to someone else, which raises serious doubts about where Amazon's $22 billion content budget is actually going. But that is not the only story in this month's data and a lot happened on the glass in March. Time to dig in.

Today at a glance:

HBO Max owned the title charts

The home screen still has room for homegrown content

The notable absents

When the home screen becomes a shop window

Amazon, the money you spend on originals belongs in your product

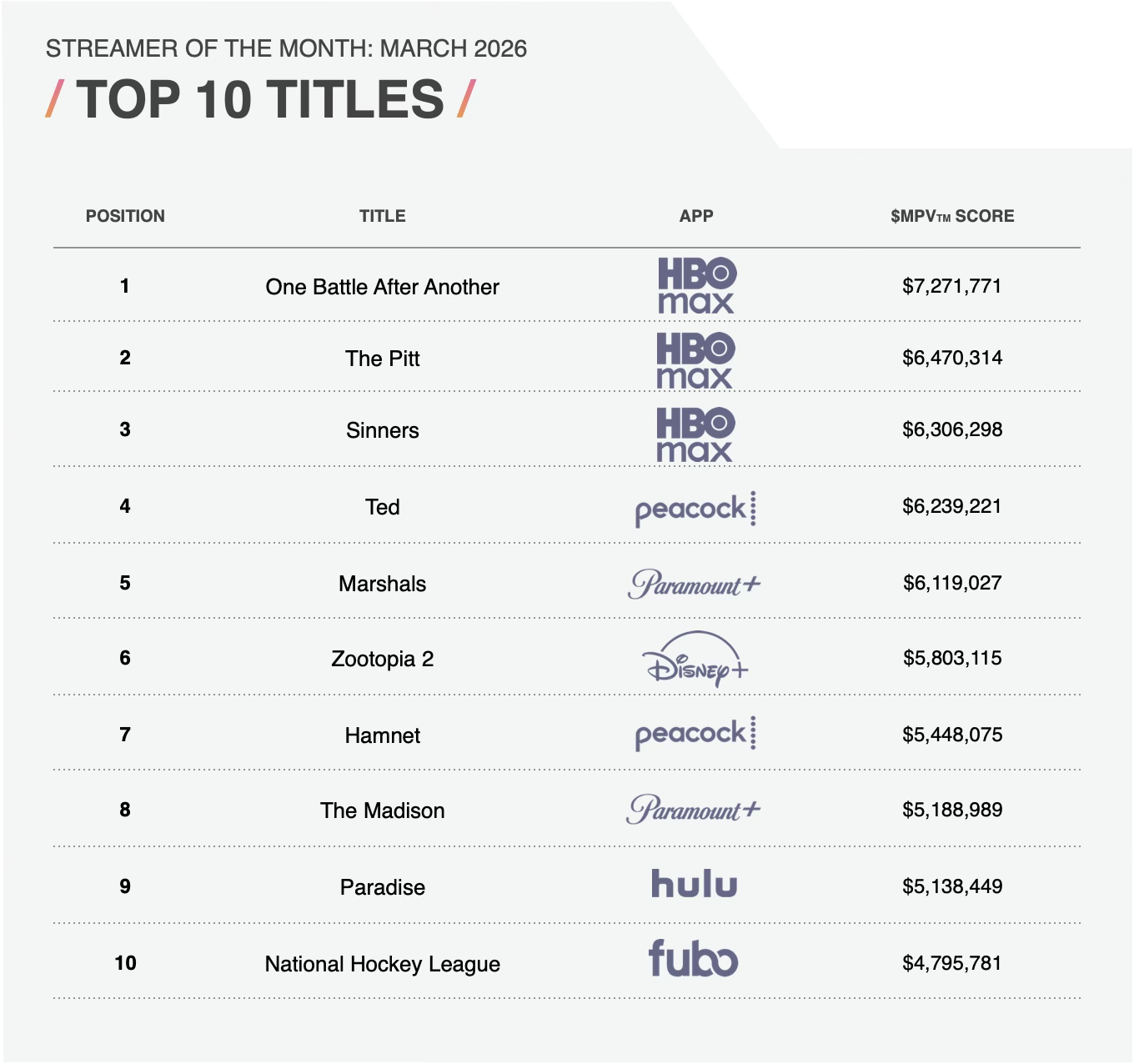

HBO Max owned the title charts

HBO Max placed multiple titles in the top 10 promoted titles chart in every market Looper Insights measured in March (except the UK as HBO Max only launched on March 26). A Knight of the Seven Kingdoms, The Pitt, One Battle After Another and Sinners appeared repeatedly across country rankings. No other content brand came close to that cross-market promotional footprint at the title level during the month.

Young Sherlock, a Prime Video original, was the one title to cut across multiple geographies in a comparable way, appearing in the top five in Australia, the UK and Germany.

Title-level placement reflects what platforms and device partners are willing to feature prominently on their home screens, which means it captures not just what a streamer is pushing but what the broader distribution ecosystem believes audiences will respond to. HBO Max content kept clearing that bar in market after market.

The home screen still has room for homegrown content

In the UK, BBC iPlayer topped the app visibility chart outright, ahead of Prime Video, Netflix and every global streamer in the ranking. Public service broadcasters claimed four of the top ten title slots across iPlayer and ITVX. In Germany, five of the top ten apps by €MPV were local or German-owned services (RTL+, Joyn, ZDFmediathek, ARD Mediathek and MagentaTV), making it the most locally competitive market in the dataset. In Australia, Married at First Sight on 9Now topped the promoted titles chart for the entire month. In Germany, ZDFmediathek placed a long-running domestic drama in the top ten. None of this looks like a market where local broadcasters are being squeezed out.

Two forces are driving this:

→ The first is the appeal of local content. Australian viewers chose a reality format on a free catch-up service over prestige HBO Max drama in March. CTV platforms are not blind to that pull. Device manufacturers and OS providers are commercial businesses and when local content demonstrably drives engagement and time spent on their platforms, they have every incentive to give it prominent placement without anyone forcing them to. The home screen position that broadcasters hold in their respective markets reflects both editorial deals and the hard commercial logic that local content keeps viewers on the platform longer and coming back more often.

→ The second is regulatory and it matters most in markets where that editorial & commercial logic alone has not been sufficient to protect local visibility. In the UK, the Media Act 2024 requires connected TV platforms to give public service broadcasters prominent, accessible placement within their interfaces and Ofcom has since published a code of practice to enforce it. PSBs submitted evidence during the process showing measurable drops in viewership when removed from visible app menu positions. Germany introduced a public value label to guarantee prominent placement for designated German services on CTV platforms, though implementation has been uneven and, as I covered previously, the result has been described as a public value corner rather than genuine integration. France created a General Interest Service status covering public broadcasters and commercial free-to-air players with a similar intent.

The notable absents

Two of the most-used platforms on any CTV device barely register in Looper Insights’ placement data across all four markets. Netflix holds a solid position in the app charts, sitting third in Australia and sixth in the UK but places almost no titles in the promoted titles charts in the US or Germany and only two in the UK. YouTube does not appear in either chart. For platforms that between them account for an enormous share of daily screen time globally, that may leave you wondering but it reflects how both platforms approach prominence.

Both Netflix and YouTube have invested heavily in a different kind of placement entirely. Netflix has for years required device makers to include (for free) a dedicated button in order to get access to its app. It demands the 1st app slot on every UI which turns opening Netflix into a reflex. Same for YouTube.

The consequence of that model is that neither platform needs to promote individual titles or invest in promotional assets for CTV home screens the way Prime Video or HBO Max do. Netflix routes discovery through its own algorithm, with research consistently suggesting that the vast majority of what people watch on the platform is found through Netflix’s own recommendation engine rather than through any external surface. YouTube operates on an even more habitual basis: viewers open it with intent to search or scroll, not because a specific video was promoted on a Samsung home screen. The content comes after the behaviour, not before it.

When the home screen becomes a shop window

March threw up another tactic, even if it only showed up in one market. In the US, Paramount+, Disney+ and AMC+ all used prominent home screen placement not to promote content but to sell subscriptions, pushing discounted offers and free trials directly on Vizio and Samsung device home screens. Paramount+ ran a $2.99 introductory offer; Disney+ and Hulu bundled together at $4.99; AMC+ offered 90 days at no cost. The home screen, traditionally the territory of content marketing, became a direct acquisition tool.

None of the European or Australian markets in the March data showed anything comparable. Home screen placement in the UK, Germany and Australia remained focused on title promotion, with price and subscription mechanics kept off the glass entirely.

Streamers in Europe navigate the same subscriber acquisition costs, the same churn dynamics and the same crowded attention economy. The US data suggests that device partners are open to that kind of promotional real estate. What remains unproven is whether a price promotion on a passive, lean-back screen drives subscription conversion the way it does on a phone or laptop, where the path from offer to checkout is a matter of seconds.

Amazon, the money you spend on originals belongs in your product

Amazon reported spending $22.4 billion on video and music content in 2025, up 10% year on year, according to its annual 10-K filing. That figure includes music licensing, which matters for context, since Netflix's $18 billion covers video only. Strip music out of Amazon’s number and the video-specific estimate may sit lower, though it still represents an enormous commitment to content at a time when the placement data keeps telling the same story: Prime Video dominates the shelf but its originals rarely dominate the chart.

Amazon can afford to spend on original content but Prime Video’s real competitive position in the streaming market is not as a content studio. It is as the world’s most powerful aggregator. Prime Video Channels earns Amazon a commission on every third-party subscription sold through its platform, housing HBO Max, Paramount+ and dozens of others behind a single login and a single bill. The more services Prime Video distributes, the more indispensable the platform becomes, regardless of whether Amazon’s own originals are winning awards or placement charts.

The sports rights strategy points in the same direction. Amazon pays approximately $1 billion per year to the NFL for Thursday Night Football and holds a share of the NBA's 11-year, $76 billion media rights deal. Live sport drives the kind of appointment viewing that makes a platform non-negotiable for a specific audience segment and generates advertising inventory that a prestige drama simply cannot match at scale. Reuters reported that Amazon has been shifting its strategic emphasis toward live sports and away from dependence on original content as its primary growth lever, with its entertainment team commissioning fewer film and TV projects since 2022.

In every market Looper Insights measured, Prime Video’s app visibility was built on distribution scale and platform presence, not on the promotional momentum of its own titles. If Amazon’s originals strategy were firing as intended, you would expect to see more of its own titles converting that shelf space into title-level placement.

None of this means Amazon should abandon original content. Tentpole titles still serve real membership acquisition and retention functions and the flywheel argument cuts both ways: a platform with nothing worth watching on its own loses credibility as an aggregator over time. But there is a reasonable case that the balance has tilted too far toward competing with Netflix on prestige drama ground, when the aggregator and sports rights model represents a structurally more defensible and differentiated position that no one else in the market is positioned to match.

Get the full picture 👇🏻

The full top ten app and title rankings across the US, UK, Germany and Australia, including placement values are available in the Looper Insights Streamer of the Month reports for March 2026. Download them below:

→ Streamer of the month Germany

→ Streamer of the month Australia

That’s it for today. Comments, shares or likes come a long way 🙏🏻

Catch up on our previous reads:

🗳️ Poll Time:

Enjoy your weekend and see you on Thursday for another edition of Streaming Made Easy!