France Télévisions bets big on YouTube

While running a €140M savings plan with 212 fewer staff than a year ago.

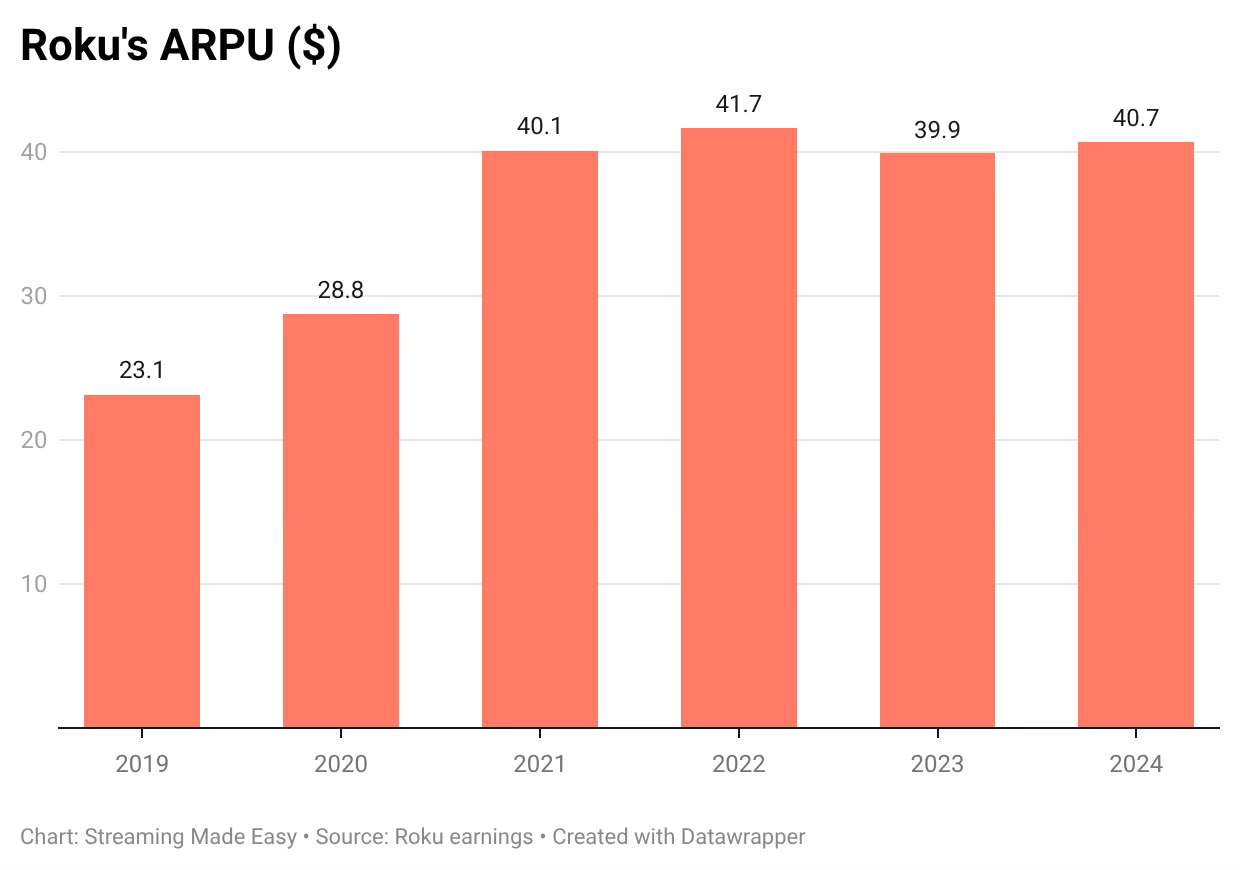

🛎️ 100M households, one missing number

I was at Roku when company walls were showcasing the 50M goal we had set for ourselves (I got a mug and cool socks when we did in 2021!). That goal was actually 50/50: 50M active accounts and 50$ ARPU.

Roku just announced it reached the 100M mark (based on active accounts over a 30-day period) so 5 years later, they’ve doubled the base but where is the ARPU at?

It seems stuck at 40$ or so, perhaps the reason why Roku stopped reporting active accounts and ARPU figures in Q1 2025 (except for the occasional milestone announcement like this one).

The question for the next five years is not just whether Roku reaches 150M or 200M households but whether it can extract more revenue from the base it has already built. Advertising alone is not closing that 10$ gap, which is exactly why Roku is pushing hard into subscriptions: Premium Subscriptions hit a record for net adds in Q4 2025, Apple TV+ joined a roster of 70-plus partners, bundles are coming in 2026 and Howdy, its own $2.99 SVOD, is expanding beyond the Roku ecosystem onto Amazon Prime Video.

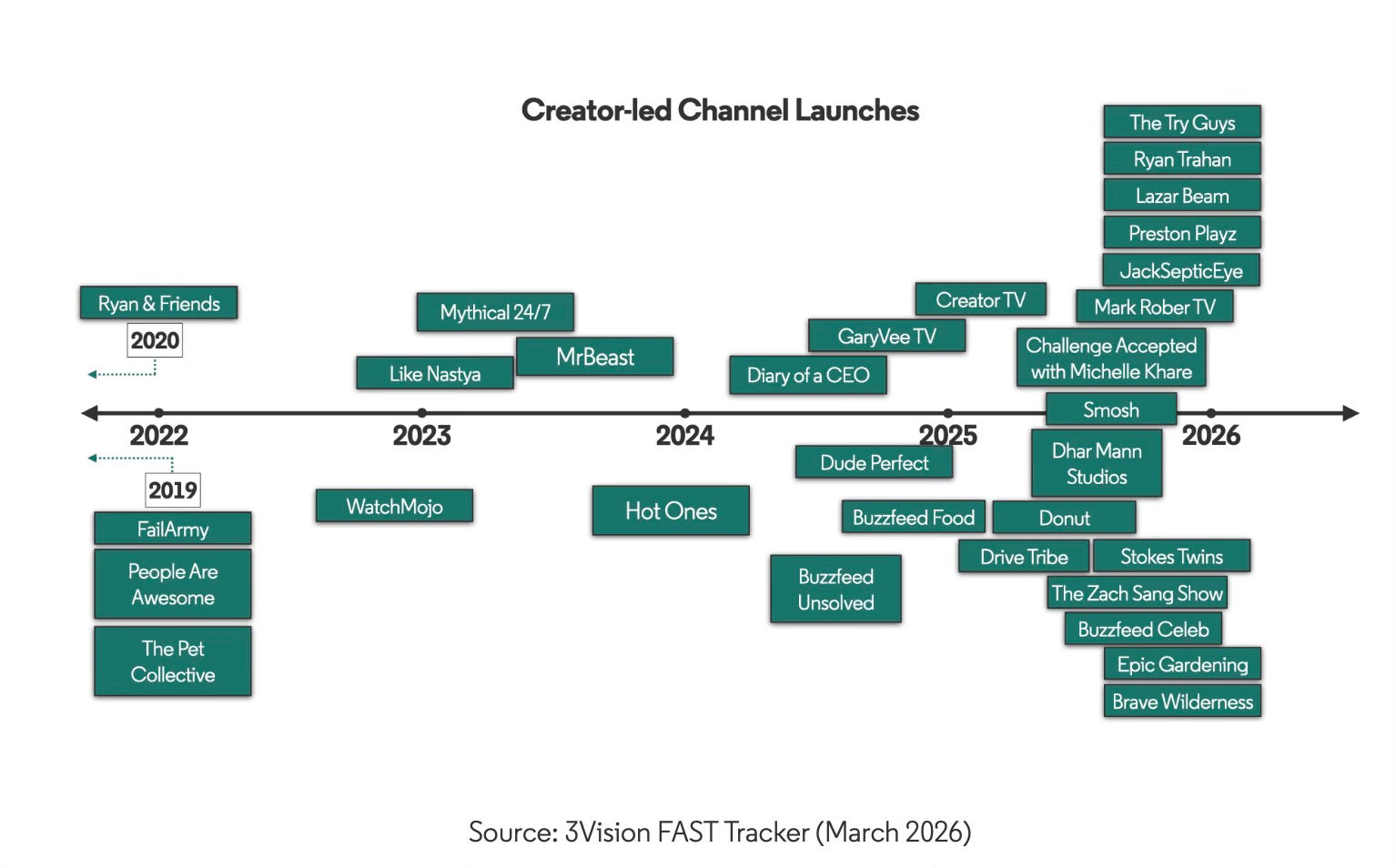

📺 Can FAST speak creator?

“Mom, we’ve linearised creators” says Olivier Levard, CEO of Full Joy Media, as he announced the launch of “House of Creators”, the latest addition to the Samsung TV Plus France line up.

Food, true crime, science, lifestyle, talk, entertainment from 11 YouTube channels and 13 content creators (L’Atelier de Roxane, Morgan VS, Louis-San, Noa, Claire, Liv, DrFeelgood, Tartin, Adem & Bilal, Les Gens d’Internet, Poisson Fécond).

”In short, it’s not an alternative to YouTube, it’s a new way to discover these talents. No algorithms. No subscriptions. No downloads. Right from your remote control, on millions of Samsung Smart TVs in France. And soon, absolutely everywhere!”

Olivier Levard, CEO of Full Joy Media

It is a premise many platforms and creators have tested over the past 3 years, platforms chasing younger viewers and creators chasing audiences beyond their existing subscriber base.

Is the bet paying off? More channels doesn’t equal success. I would argue we’re still in the test and learn phase and I tend to agree with Gavin Bridge, from The FASTMaster, in his latest piece, and see a brighter future for creators inside on demand platforms like Tubi and Netflix.

“The existential challenge facing FAST is generational. The format was built for, and has been captured by, an older demographic with the behavioral habit for passive linear viewing. Gen Z and younger Millennials are not going to navigate an 600-channel EPG. They already have their answer — it’s a swipeable feed, algorithmically curated, capped at a fraction of what legacy platforms currently carry. FAST either meets them there or cedes that audience permanently to TikTok and Twitch.

This requires a radical rethink: not incremental pruning, but a fundamental reinvention of how channels are programmed, how grids are presented, and what FAST is actually for.”

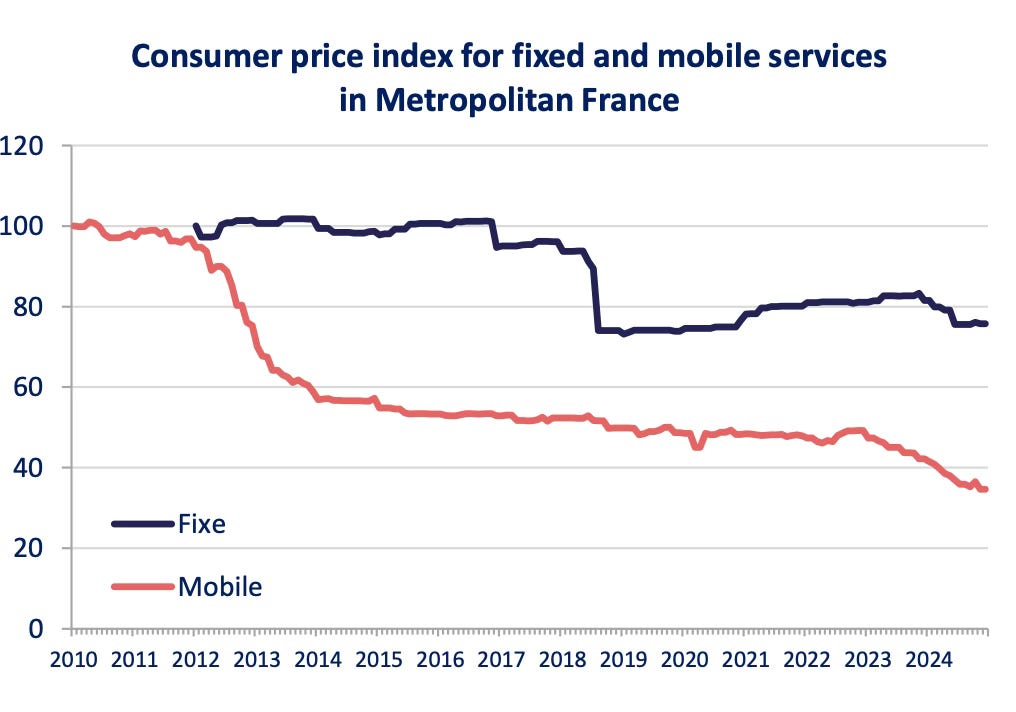

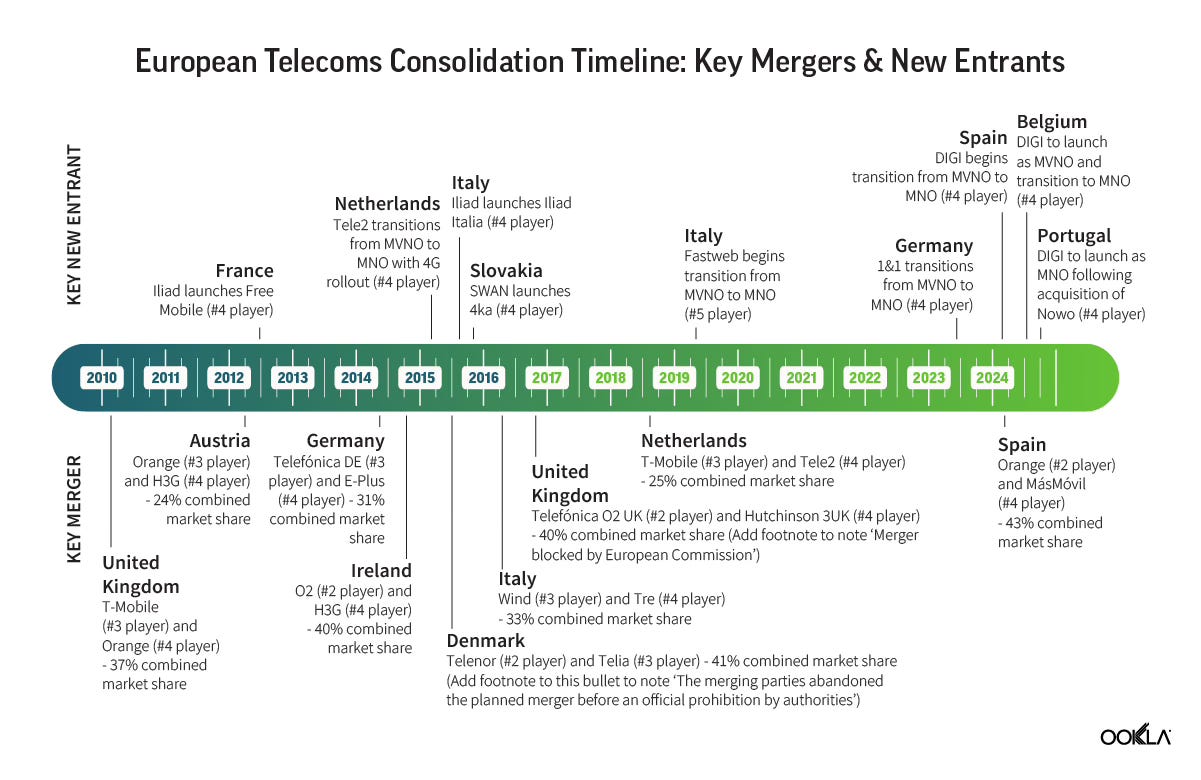

☎️ The race to three

France could be on the verge of becoming a 3-player market again. Ever since Free entered the market in 2012 (with a very disruptive pricing strategy incl. a 2€ per month mobile subscription), the French telecom market has been competing heavily on price.

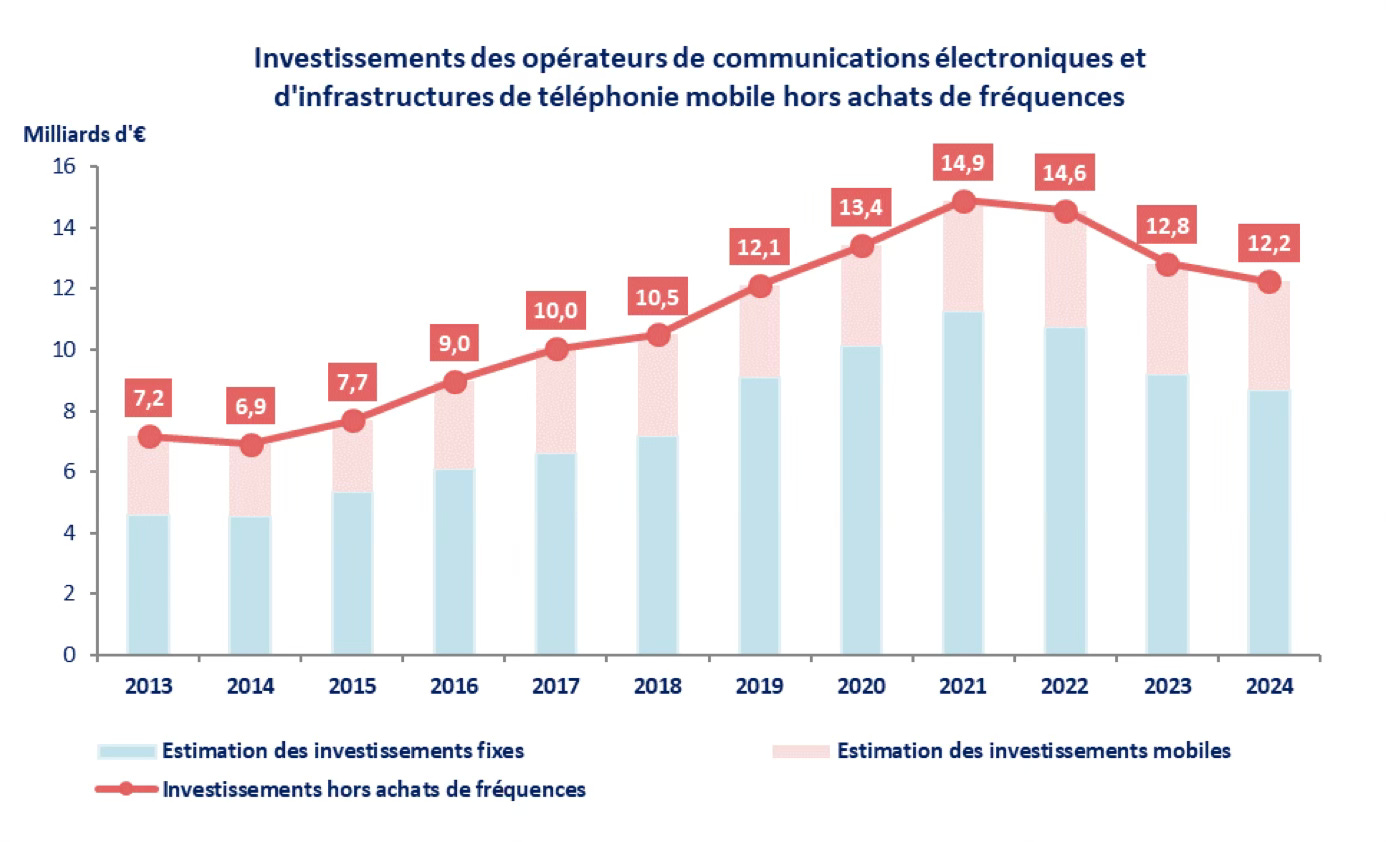

Yet French operators still managed to keep investing but current pricing dynamics are unsustainable for funding network investments, particularly as 5G adoption accelerates and data consumption grows.

Hence why Orange, Free and Bouygues have upped their bid to buy SFR (from 17B to 20.35B€) and now have an exclusive window (until May 15) to close the deal.

This is the latest consolidation trend we’re seeing in the region. The UK already went from four to three operators following the Vodafone / Three merger in 2025 (which took two years to get approved!). France, Spain, Germany and Italy still have four-player mobile markets.

European competition authorities seem to be more open to consolidation (despite the potential risk on consumer pricing) suggesting large-scale investment in networks to support digital transformation and improve coverage is a must have.

What will the French market look like post-purchase?

→ B2B segment: Bouygues Telecom takes the entire enterprise business and customer base.

→ B2C segment: Consumer customers will be shared between all three operators. The how isn’t known yet.

→ Mobile network in less dense areas: Bouygues Telecom acquires SFR’s rural/non-dense mobile network exclusively. This gives Bouygues significant rural coverage advantages.

→ Other infrastructure and spectrum: Shared between all three operators, including fiber infrastructure and frequency licenses.

France is not a special case, the European telco map is being redrawn, one merger at a time.

🗓️ SME Live Tickets: Early bird tickets to attend our next Streaming Made Easy Live event in Amsterdam on September 10th, 2026, are now on sale here. Premium subscribers get 30% off so consider upgrading today.

🇩🇪 Germany's new video giant

It took less than a year for the RTL / Sky merger to get regulatory approval, sign that European regulators are conscious of the extreme competition local players face from global players and that there’s no time to waste.

What happens next? One big unknown is whether RTL will eventually fold Sky, WOW and RTL+ into a single master brand or keep them separate under one corporate roof and then orchestrate upsell / cross-selling strategies amongst them. I wouldn’t want to be the marketer who will be selling today’s existing 12 distinct packages…

My best guess is that WOW will be folded into RTL+ to become the most premium tier. Sky will remain as a standalone but the tiering structure will need to be simplified and again RTL+ could be the entry point offers while Sky keeps the high-end subscriptions.

Can RTL’s mass-market instincts coexist (and thrive) with Sky’s premium ethos? If they pull it off, they’ll have the most complete video business in German-speaking Europe: news, soaps, prestige dramas, live sports, all under one roof and able to flex between Free, Pay and hybrid. If they mismanage it, they risk eroding Sky’s premium edge and unsettling subscribers giving rivals fresh ground to poach viewers.

Either way, the hard work starts now.

→ More here about the new leadership changes here.

🎙️StreamTV Europe Unplugged

👉🏻 APPLE PODCASTS | SPOTIFY | YOUTUBE | DEEZER with more platforms here.

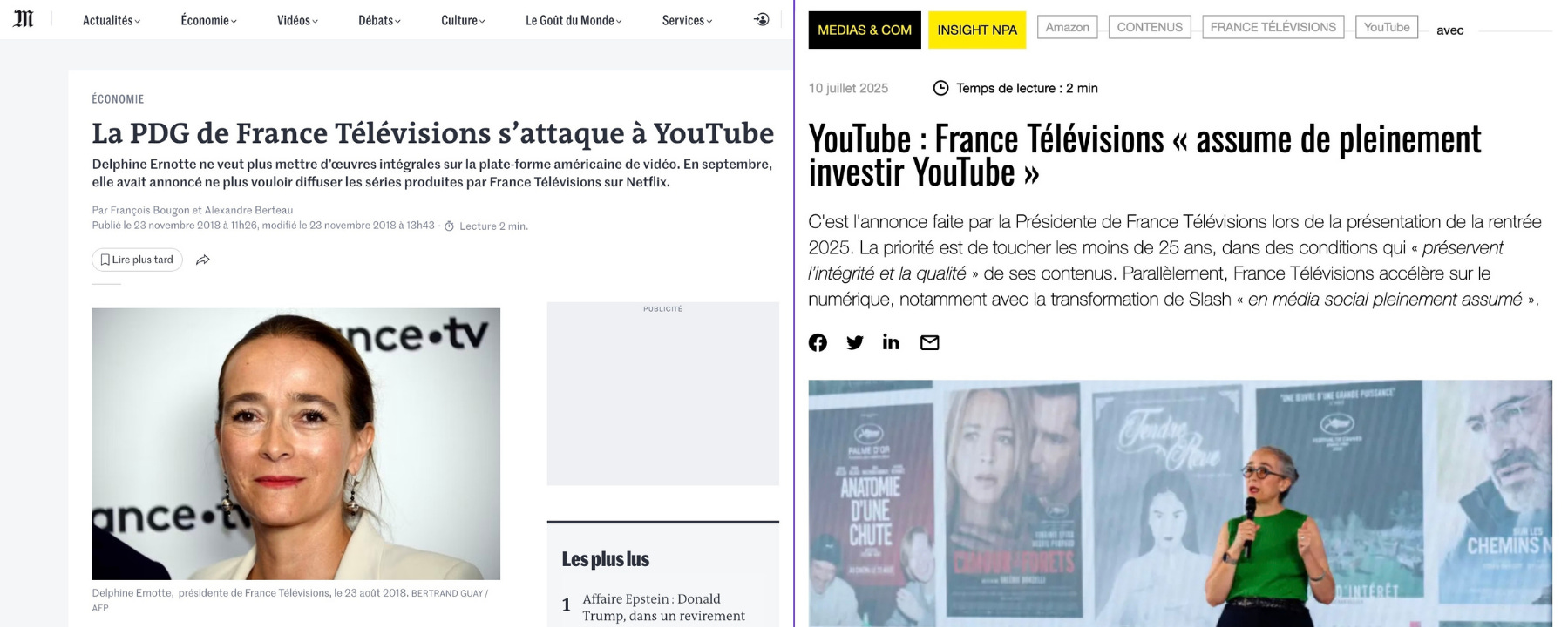

🇫🇷 The broadcaster who learned to love YouTube

In July 2025, Delphine Ernotte, President of France Télévisions, signalled a change of tactic. Seven years after publicly dismissing YouTube as a threat, she announced plans to invest fully in the platform across all content types, from documentaries and magazines to drama, with a priority on reaching viewers under 25.

Now, the group didn’t start on YouTube in 2025 given how extensive their YouTube portfolio already is.

The partnership announced this week covers news content exclusively, meaning the full slate of national and local bulletins, daily and weekly magazines and investigation programming from France 2, France 3, France 5 and France Info. Around 20,000 hours of content per year, available on YouTube shortly after broadcast. For context, CMA Média signed a similar deal earlier this year covering roughly 1,000 hours annually.

News as the entry point makes sense. It is already the dominant genre in FTV’s existing YouTube footprint by channel count, subscriber numbers and views. Going bigger on news is the logical extension of the “streaming first” strategy and with the French presidential election approaching, the stated disinformation angle gives the partnership a public service wrapper that is hard to argue with, whatever you think of YouTube’s actual track record on the subject.

The ad model deserves attention. Unlike a standard YouTube partner arrangement, France TV Publicité retains direct control of its inventory on the platform, commercialising it independently rather than ceding revenue to Google. That is a win, though how much it yields at scale remains to be seen.

The harder question is execution. Getting 20,000 hours of existing content onto YouTube annually, organised into coherent thematic and IP-based channels rather than a bulk dump, is an operational commitment for a group running a €140M savings plan with 212 fewer staff than a year ago.

YouTube is also a hands-off major platform. It provides tools like Likeness ID (included in this deal to protect journalists and presenters from AI-generated impersonation) but the idea that a public broadcaster can meaningfully fight disinformation from inside a platform that runs on algorithmic amplification, without structural commitments from YouTube beyond tooling, is a bet that will need proving.

As we've seen from the six-month parliamentary commission led by Charles Alloncle, every move FTV makes is being scrutinised for either bias or wastefulness, often both at once. A high-profile YouTube partnership that fails to reach younger audiences, gets entangled in a disinformation incident or hands the algorithm editorial control in practice will give critics who need very little encouragement exactly what they are looking for.

That’s it for today but before you go:

🗳️ Poll time

🗓️ SME Live Tickets

Early bird tickets to attend our next Streaming Made Easy Live event in Amsterdam on September 10th, 2026, are now on sale here. Premium subscribers get 30% off so consider upgrading today.

That’s it for today. Enjoy your weekend and see you on Tuesday for a Deep Dive edition of Streaming Made Easy Premium.