The premium layer hiding under Roku's free funnel

The Roku Channel hit 3% of all US TV viewing. Its premium subscriptions business is the under-discussed layer sitting on top of that free funnel.

Consumers did not kill the bundle. They rebuilt it themselves.

What used to be a handful of fat cable packages is now an overwhelming mix of ad tiers, FAST channels, AVOD corners and premium subscriptions that all live on the same home screen. Roku sits underneath the streaming ecosystem as an operating system, an ad platform and a marketplace.

The Roku Channel is where those roles converge. It blends free ad‑supported linear channels (FAST), AVOD, third‑party premium subscriptions and even Roku’s own SVOD like Howdy into a single environment. When a viewer opens The Roku Channel on a Roku device, they are not choosing between “free” and “paid” universes. They are moving along a single funnel: drop into a free channel, click into an on‑demand title, hit a paywall for a premium add‑on, all without leaving Roku’s UX or billing layer. For streamers, that means your SVOD offer lives directly on top of a very large free TV audience. For Roku, it means every hour of free viewing can be monetised twice: once with ads and again if the viewer upgrades into a subscription.

In this edition, I want to focus on that premium layer: Roku’s US Premium Subscriptions marketplace, which is often under‑discussed when people explain Roku’s rise in Nielsen’s The Gauge purely through AVOD and FAST. We will look at its content mix, its pricing logic and how Roku's advertising thesis shapes the premium storefront

The dataset covers 72 premium subscriptions available via Roku in the US as of February 2026 and you will see plenty of charts you can reuse to pressure‑test your own distribution strategy.

Today at a glance:

Why The Roku Channel matters

72 services, unpacked

Pricing, mapped

What’s missing

Roku’s advertising thesis (and what it means for premium services)

Why The Roku Channel matters

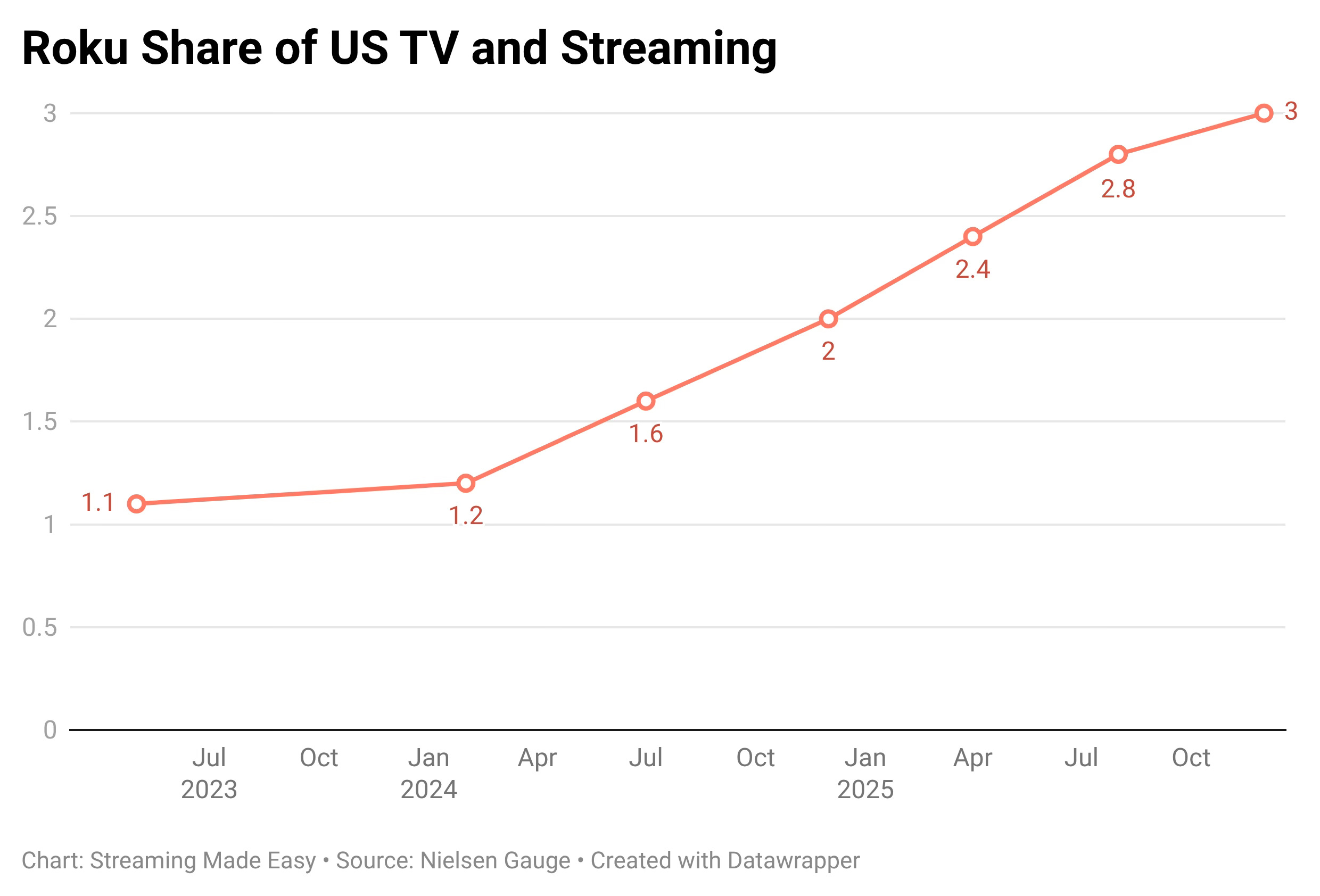

The Roku Channel went from zero in 2017 to 3% of all US TV viewing by December 2025 (up 45% year over year and 190% versus December 2023). To put that in perspective: only 4 other streaming services have ever crossed the 3% threshold in Nielsen’s Gauge (YouTube, Netflix, Disney’s services and Prime Video). The Roku Channel now sits in that company.

At the platform level, Nielsen’s Gauge data shows that Roku-powered devices accounted for just over 21% of all U.S. TV viewing time by late 2025, a share big enough to put Roku OS ahead of cable and on par with or above broadcast.

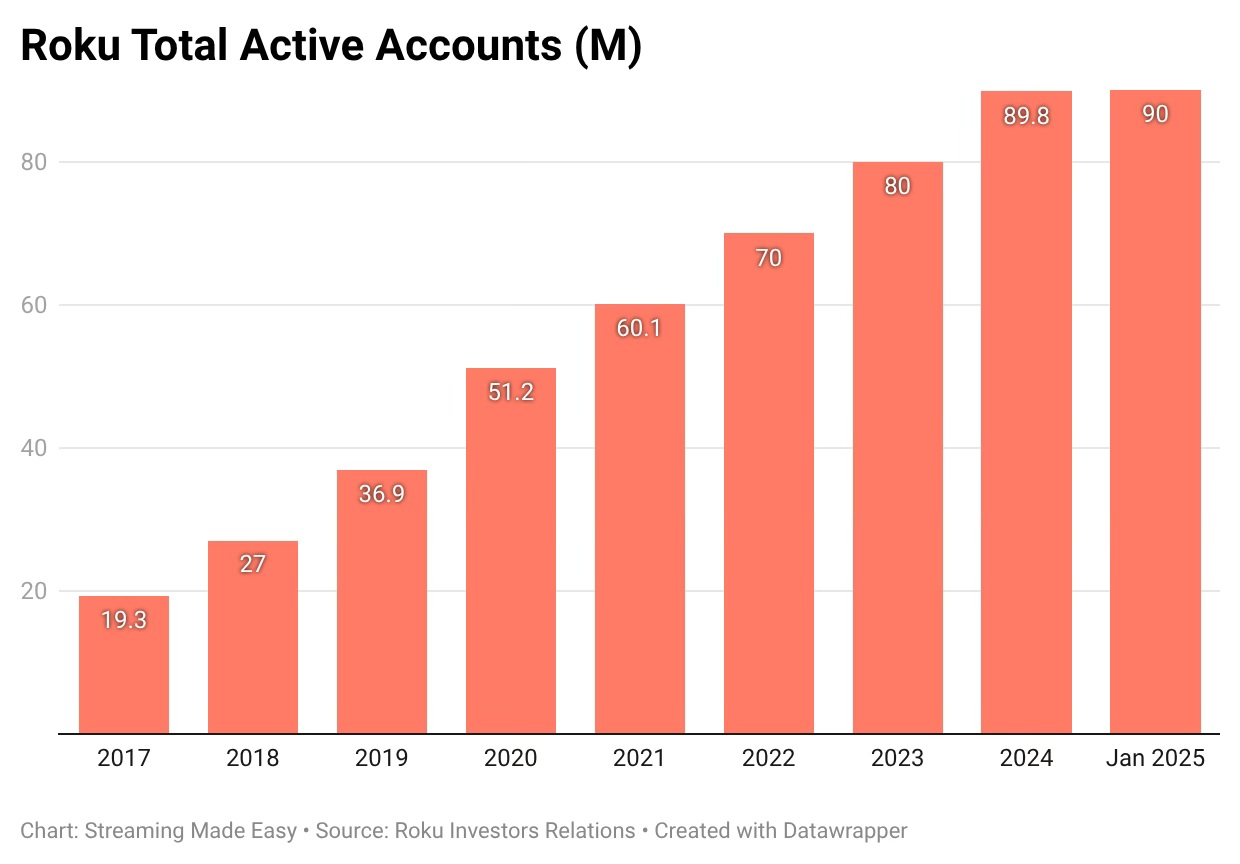

By the end of 2024, The Roku Channel app was reaching U.S. households representing nearly 145M people and ranked among the top three apps on the platform by reach and engagement, with streaming hours on the channel up 82% year over year (see the Roku Q4 2024 shareholder letter). Throughout 2025, The Roku Channel even hit the n°2 app spot on the platform in the U.S. by engagement with close to 90% of that viewing now coming from Roku Experience entry points (most notably their Home Screen content row) rather than people manually opening the app tile.

The real power of The Roku Channel lies in its hybrid business model. According to Roku and Horizon’s FAST study, 64% of U.S. Roku households stream FAST on Roku and if you aggregated all that FAST viewing into one app, it would be the fourth‑largest app on the platform by reach (according to the Horizon / Roku “FAST is Vast” report). In plain English: free, ad‑supported channels are one of the main ways people enter and spend time inside Roku’s environment.

That matters directly for SVOD. The same research shows that roughly two‑thirds of SVOD viewers on Roku are now “ad‑light” meaning they still pay for subscriptions but also watch ad‑supported content. For a premium subscription sitting inside The Roku Channel, FAST is not a separate universe, it is the top-of-funnel. Roku uses its Home Screen rails and free channels to generate hours of low‑friction viewing, then pushes those viewers toward higher‑ARPU outcomes: premium add‑ons including Roku’s own SVOD Howdy or newly acquired Frndly TV.

In May 2025, Roku indeed paid $185 million to acquire Frndly TV, which offers a low-cost live TV bundle with 50+ channels (Hallmark, A&E, History, Lifetime) starting at $6.99 per month. The deal closed in Q2 2025 and Frndly TV became a default app on new Roku devices. This is Roku buying its way into the vMVPD space, sign that it sees value beyond pure ad monetisation.

For specialty streamers trying to figure out where to plant their flag, that strategy matters. Amazon Channels offers the Prime membership engine, with U.S. subscriber estimates often cited around 180M and case studies like Antenna’s Apple TV+ via Amazon Channels to show how much volume a marketplace can drive. Roku offers raw scale with no barrier to entry: no membership required to browse The Roku Channel’s free tiers.

72 services, unpacked

The Roku Channel’s (aka TRC) US premium subscriptions catalog is compact but focused. As of February 2026, TRC offers 72 premium subscriptions (for comparison Amazon Channels has 124 services) broken down as follows: