Canal+ swoops into Belgium

They left in 2004. Now they're back and this time they brought the Champions League.

🔎 Streamers are finally showing up where viewers now start

Kinda cool to see the 1st two video players confirming one of my 2026 predictions, that is to figure out to exist and be discovered in the era of GEO and LLMs.

Similarweb’s 2025 Generative AI report found that AI platforms generated over 1.1 billion referral visits in June 2025, up 357% year over year. Consumers now start their journeys inside AI assistants, asking questions and shaping preferences before they ever reach a streaming app. A recent Adobe Express survey reports that 77% of Americans who use ChatGPT treat it as a search engine, with 24% choosing it before Google. The next generation of viewers may never type “what should I watch” into Netflix or others. They will ask ChatGPT, Perplexity or Gemini and go wherever the answer sends them.

Streamers should design their GEO (Generative Engine Optimization) strategy now. The new must have App Store may be nested in ChatGPT and its peers. When ChatGPT first launched its App Store, video players were MIA. Now, Tubi and M6+ (the streaming platform of commercial broadcaster M6) have launched their own native apps.

What does it do? It’s a content discovery companion.

Is it perfect? No as evidenced below with the M6+ native app which suggests titles that aren’t movies when I asked for a specific movie recommendation.

Or with Tubi where I was downgraded to a lower model due to lack of credits and the query ultimately went nowhere (could be that it’s because I’m not in a Tubi market).

Regardless, it’s a step in the right direction versus the movie recommendation prompt that takes you nowhere. Expect every major streamer to have its own app by year end.

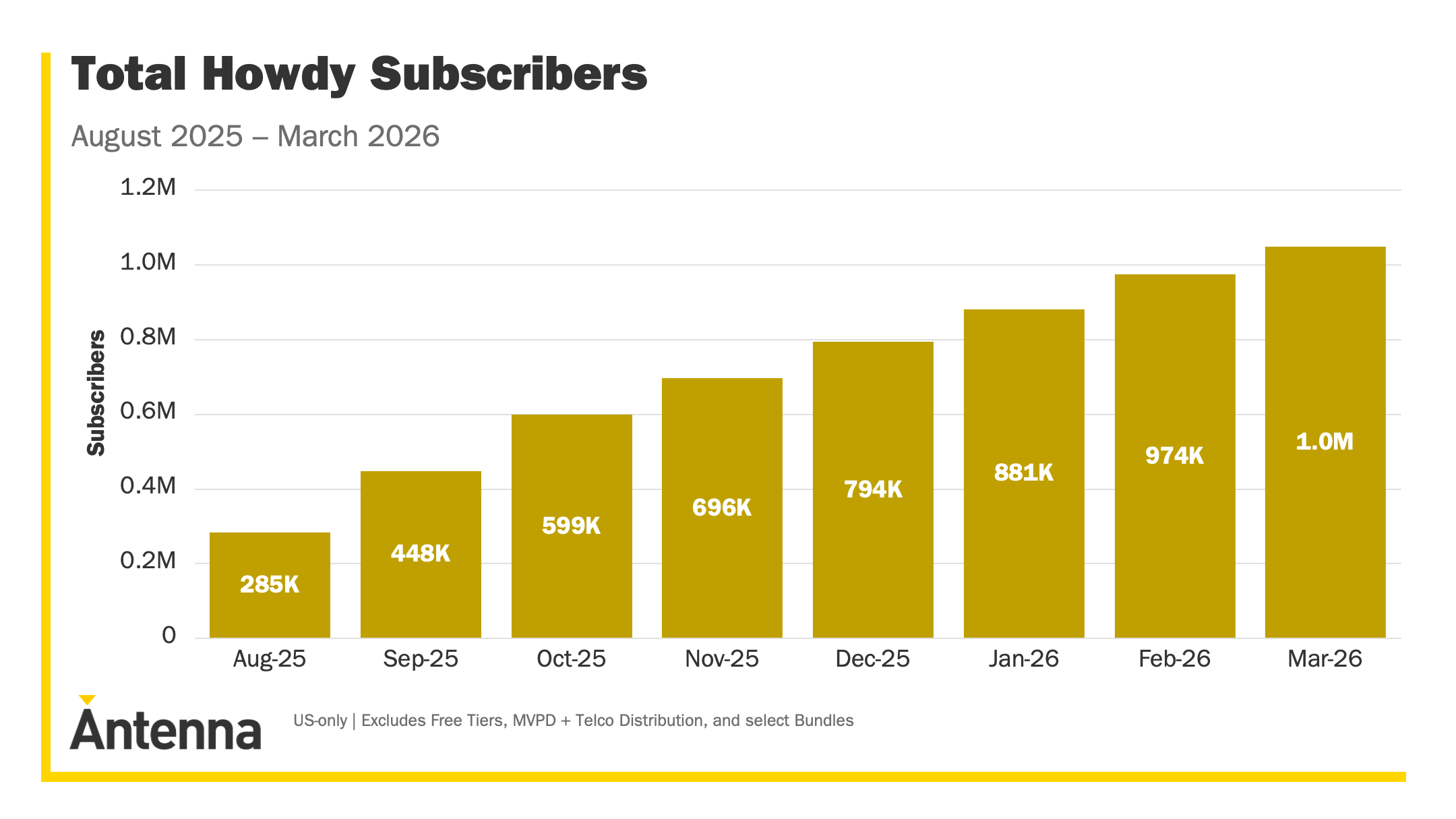

🤠 Howdy surpasses the 1M mark

No one understood this move when Roku launched Howdy in August 2025: $2.99 a month, ad-free movies and TV, available only through The Roku Channel. The content felt like a repackage of what was already sitting in Roku’s AVOD library, hard to see the logic.

Eight months later, Antenna estimates Howdy has surpassed 1M subscribers. It added nearly 300K in its first month alone, then held above 100K new subscribers every month after that.

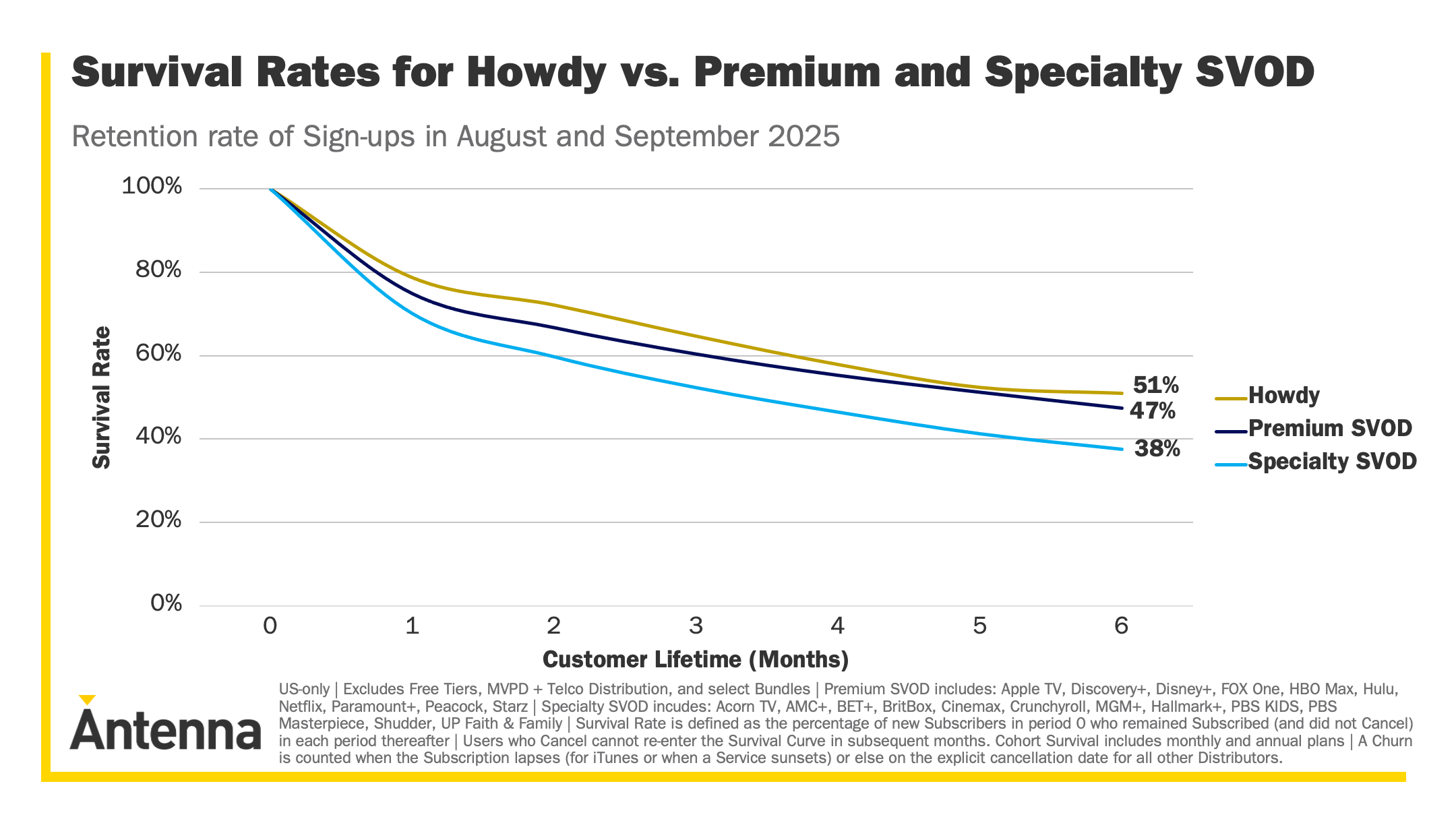

Among people who signed up in August and September 2025, 51% were still subscribed 6 months later. That sits ahead of the Premium SVOD average of 47% and well ahead of the Specialty SVOD average of 38%. The $2.99 price point does a lot of work here: low monthly commitment means less friction at the moment churn decisions get made.

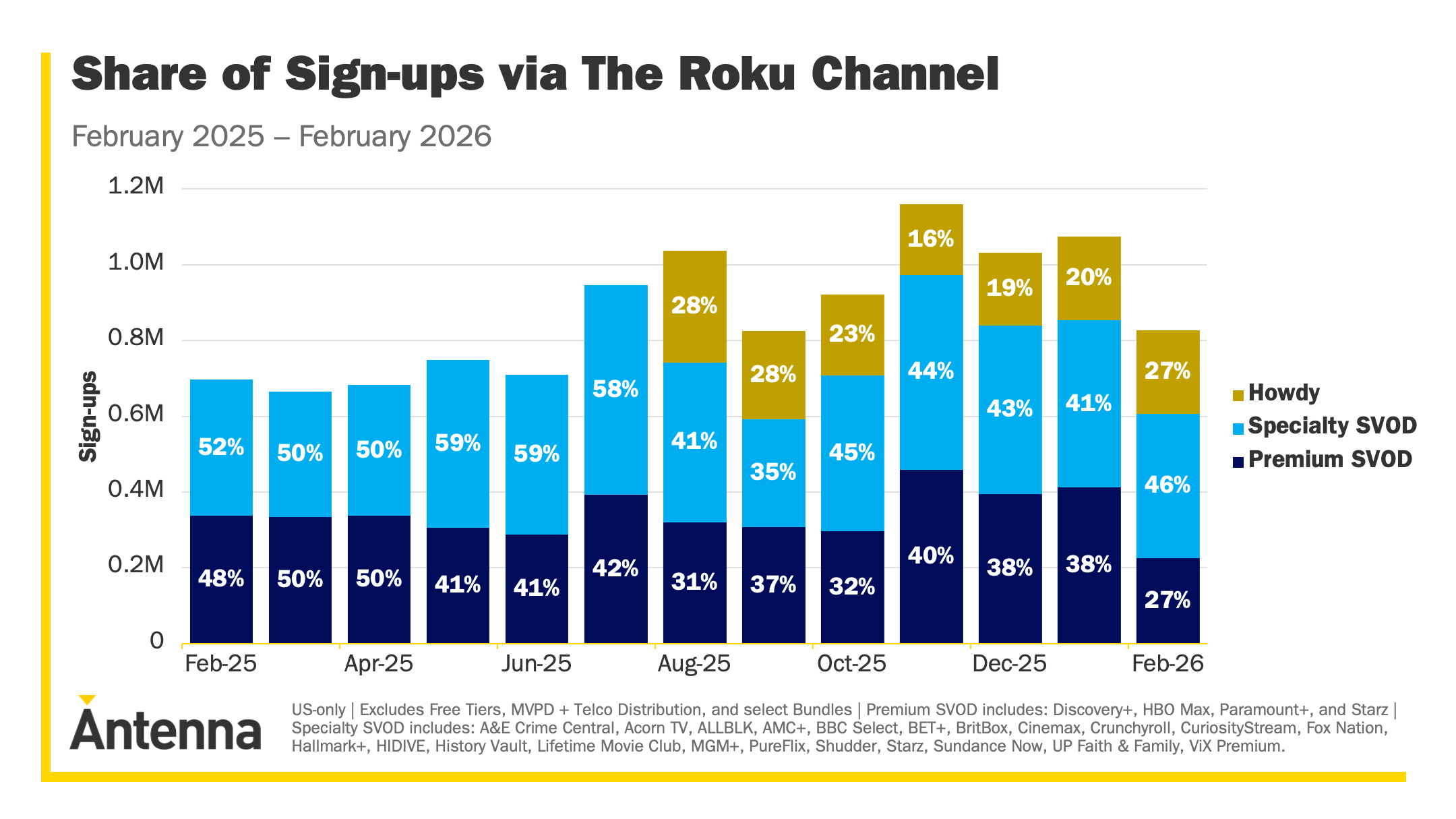

The distribution strategy matters too. Howdy accounted for 23% of all SVOD sign-ups via The Roku Channel since launch. When you're the number one platform in the US with 44% of all connected-TV streaming hours you know how to convert free users into paying subscribers, a $2.99 product is is the “easiest” upsell in streaming.

In March, Howdy launched on Amazon Prime Video Channels, the one distribution platform with comparable scale and arguably superior billing infrastructure. If Howdy holds its retention numbers on Amazon’s platform, Roku will have proven something important: that its content library has standalone value beyond its own ecosystem.

For more on Roku’s premium strategy 👇🏻

N.B: Antenna’s methodology: Antenna tracks “data from a variety of data collection partners which contribute millions of permission-based, consumer opt-in, raw transaction records. These are derived from digital purchase and cancellation receipts, consumer subscription signals, credit, debit and banking data. Antenna cleans and models this raw data, and then subsequently weighs the panel to correct for demographic and behavioural skews”. The words permission and opt-in matters as this means Howdy could have even more subscribers (since consumers can refuse to share their transaction information).

🇪🇸 Spain's creator economy means business

Spain has 285,000 active influencers on Instagram and TikTok alone. Of those, 15,000 have over 100,000 followers and 13,600 work as creators full-time. Advertisers are following: influencer marketing investment in Spain hit 158 million euros in 2025, up 25.9% year on year and double what it was in 2023.

Those numbers come from a new report by 2btube and Favikon. Gaming and streaming creators dominate by audience size. TikTok grew sponsored content volume 73% year on year, outpacing Instagram’s 45% and the average professional creator now pulls from 4.6 income streams, which looks a lot less like a side hustle and more like a small media company.

Fascinating to see that Spain has created a mandatory registry for creators earning over 300,000 euros annually with at least a million followers.

A mandatory registry, double-digit ad growth, creators running 4.6 income streams, it’s time you go discover Spain's creator economy ecosystem here.

🗓️ SME Live Tickets: Early bird tickets to attend our next Streaming Made Easy Live event in Amsterdam on September 10th, 2026, are now on sale here. Premium subscribers get 30% off so consider upgrading today.

🎙️Half an hour with the micro drama guru

👉🏻 APPLE PODCASTS | SPOTIFY | YOUTUBE | DEEZER with more platforms here.

💸 Amazon, the money you spend on originals belongs in your product

Amazon reported spending $22.4 billion on video and music content in 2025, up 10% year on year, according to its annual 10-K filing. That figure includes music licensing, which matters for context, since Netflix’s $18 billion covers video only. Strip music out and Amazon’s video-specific commitment sits lower, though it still represents an enormous number at a time when placement data keeps telling the same story: Prime Video dominates the shelf but its originals rarely dominate the chart.

In every market Looper Insights measured, Prime Video’s app visibility was built on distribution scale and platform presence, not on the promotional momentum of its own titles. If Amazon’s originals strategy were firing as intended, you would expect to see more of its own titles converting that shelf space into title-level placement.

None of this means Amazon should abandon original content. Tentpole titles still serve real membership acquisition and retention functions and the flywheel argument cuts both ways: a platform with nothing worth watching on its own loses credibility as an aggregator over time. But there is a reasonable case that the balance has tilted too far toward competing with Netflix on prestige drama ground, when Prime Video’s real competitive position is not as a content studio but as the world’s most powerful aggregator.

Get the full picture 👇🏻

The full top ten app and title rankings across the US, UK, Germany and Australia, including placement values are available in the Looper Insights Streamer of the Month reports for March 2026. Download them below:

⚽️ Canal+ swoops into Belgium

Back in November 2025, Canal+ renewed exclusive French broadcast rights to all UEFA club competitions (Champions League, Europa League, Conference League) through 2031, extending beyond their current deal through 2027.

This week, Canal+ went one step further and acquired rights across multiple European markets including Poland, Austria, Switzerland and Belgium, solidifying its position as “the largest broadcaster of UEFA Men’s Club Competitions in Europe” with rights in over 50 countries.

The most surprising move was Belgium, a country where Canal+ hasn’t operated in since they left it back in 2004. According to local sources, this was a complete left field move local operators didn’t expect, even Disney+ (initially announced as the bid winner) saw Canal+ barging in. Belgium shifts from a multi-broadcaster model to Canal+ holding 100% exclusive rights across all three UEFA competitions for 2027-2031.

Earlier this year, Canal+ made several nominations at Canal+ Benelux & Central Europe. No doubt that team has been hard at work to win these rights in Belgium and will now work towards a market launch in 2027. I believe Canal+ will use the 2023 relaunch in the Netherlands as the blue print for this Belgian market entry. It’s a streaming first approach mixing live TV channels, sport, movies & series (incl. all the Canal+ original content).

In order to compete with local Pay TV & SVOD players, Canal+ opted for much lower subscription prices (than what we typically see on the French market). Now premium football rights could justify the introduction of a higher priced tier in Belgium.

Now Belgium is not the Netherlands though: two language communities, two media markets. Proximus and Telenet will be must have partners for Canal+. The 2027 launch gives Canal+ roughly one year to build distribution, sign operator deals and localise. That’s tight for a market they haven’t touched in 20 years.

At the European level, Canal+ is attempting what Sky tried and couldn’t pull off: becoming a pan-European Pay TV & SVOD champion. The Champion’s League is definitely the right way to achieve that.

That’s it for today but before you go:

🗳️ Poll time

🗓️ SME Live Tickets

Early bird tickets to attend our next Streaming Made Easy Live event in Amsterdam on September 10th, 2026, are now on sale here. Premium subscribers get 30% off so consider upgrading today.

That’s it for today. Enjoy your weekend and see you on Tuesday for a Deep Dive edition of Streaming Made Easy Premium.