Spain's Free Streaming map

Who's leading, who's growing and what the data finally tells us

When people talk about European Free Streaming, the conversation often defaults to the UK and Germany. Bigger ad markets, more established infrastructure, more familiar to US-headquartered platforms deciding where to expand next. Spain rarely gets top billing which is a mistake. Spain has built one of the most active free streaming cultures on the continent, with adoption rates that leave its Western European neighbours behind. The UK and Germany have scale but Spain has momentum and right now momentum is the more interesting story for us here at Streaming Made Easy.

Today at a glance:

Why Spain matters right now

The Free Streaming map

How Spaniards feel about ads

The SVOD cannibalisation signal

The latest entrant: Prime Video goes free in Spain

What this means for the platforms that own the home screen

Not a premium subscriber yet? This is a good one to upgrade for.

Why Spain matters right now

Hard data on European markets is still surprisingly scarce. Spain could become the exception thanks to recent Omdia findings and GECA’s FAST Barometer, now in its third wave in under a year.

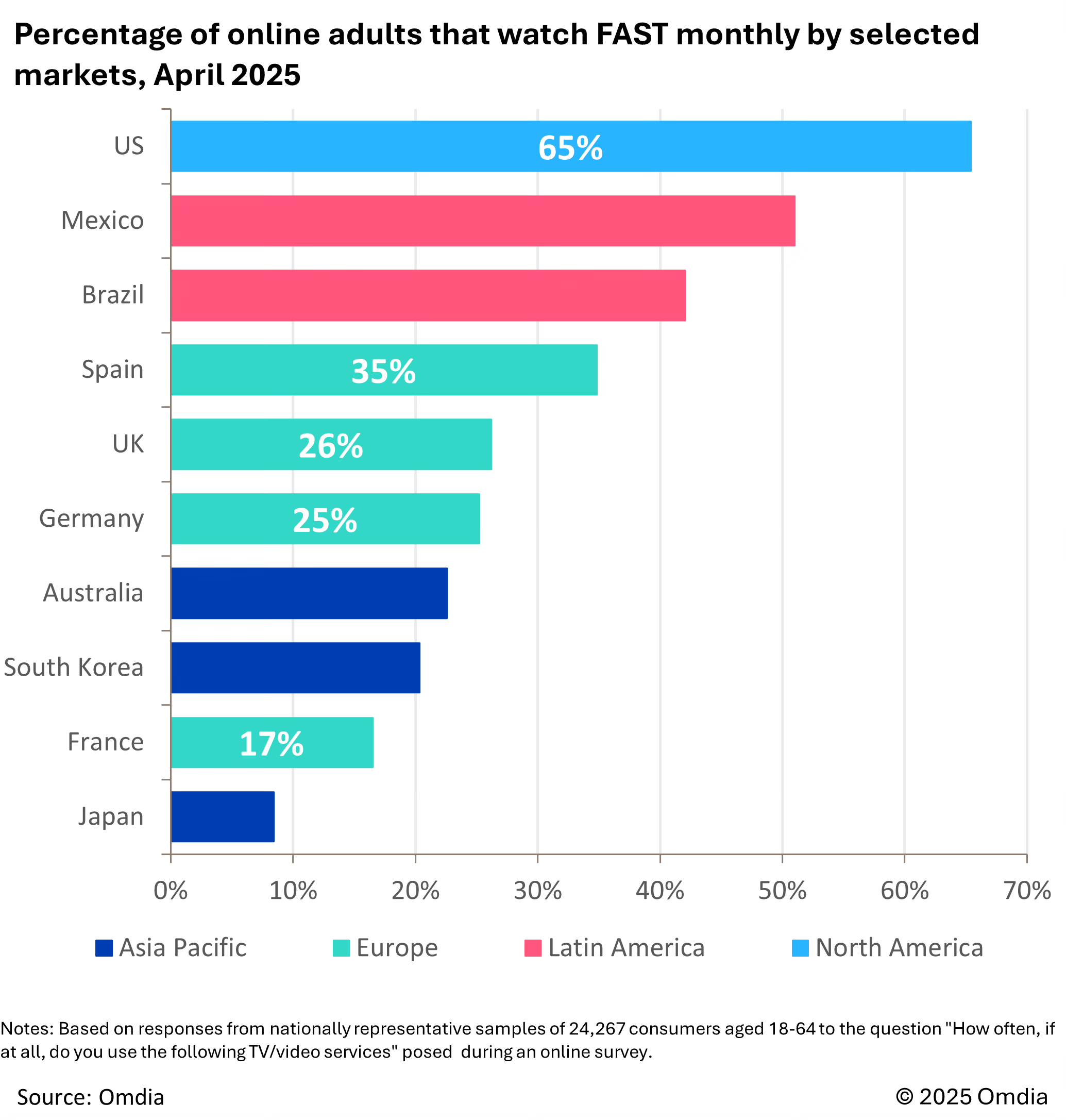

According to Omdia, monthly FAST usage in Spain sits at 35% of adults and FAST revenues are forecasted to reach $32 million in 2025 and nearly double to $65 million by 2030.

“That Spain leads Europe in FAST consumption is no coincidence. According to Omdia’s data and our own analysis at GECA, the Spanish market possesses a uniquely favourable architecture for this model: high penetration of free platforms, a robust presence of national broadcasters and a highly active connected TV ecosystem. These elements have converged to create an environment where free, ad-supported content is no longer just a supplement to subscription streaming, but a structural pillar of the broader audiovisual landscape.”

Rafael Herrera, Barometer OTT & FAST Director, GECA.

GECA goes further tracking penetration across 20+ individual platforms. Their FAST Barometer consists of quarterly surveys of 1,000 Spanish free platform users (aged 18+) to understand how they consume free video content and on which platforms.

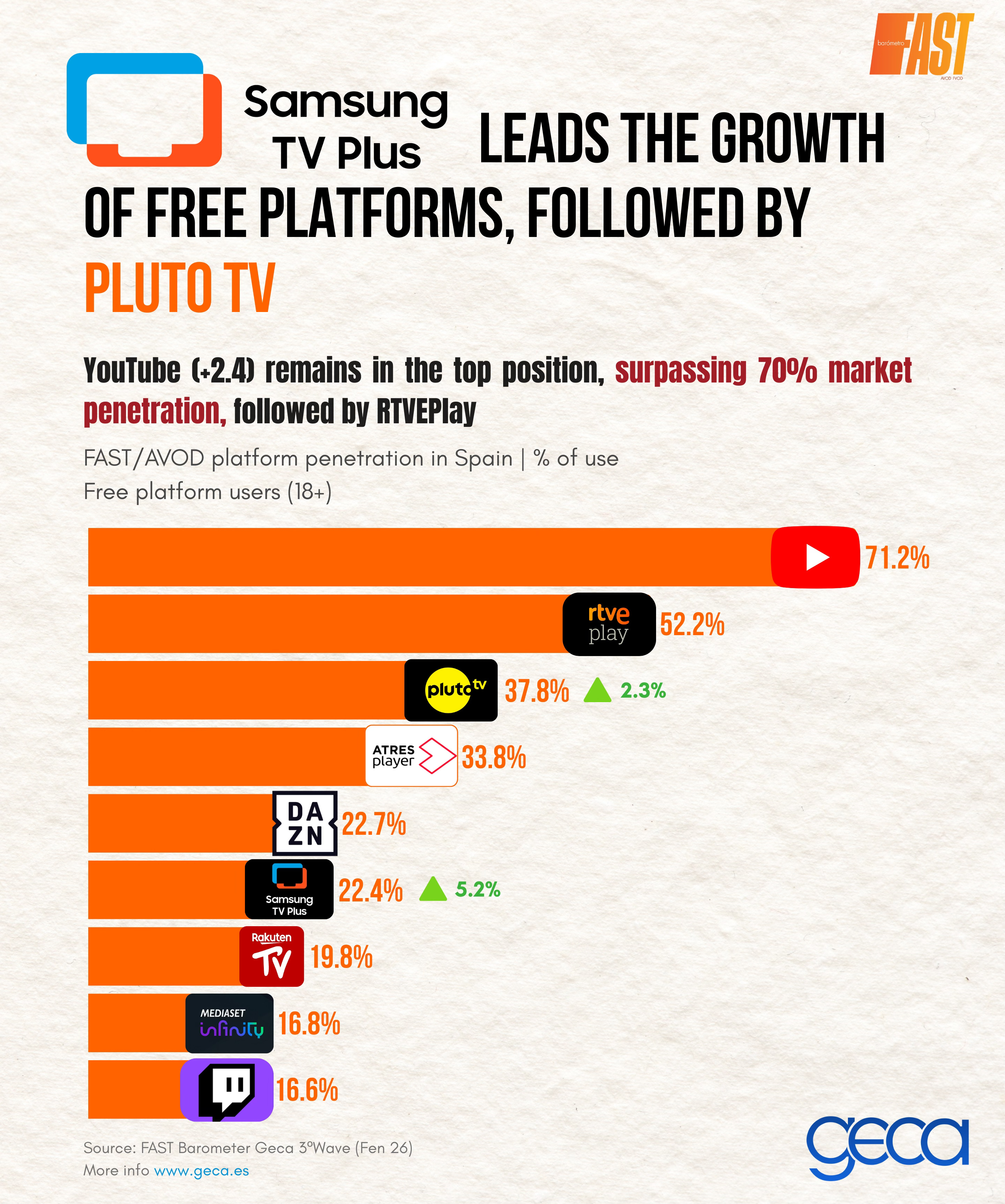

The Free Streaming map

The competitive landscape splits into four segments, each operating on a different logic.

The local broadcasters:

→ RTVE Play (the public broadcaster) sits at 52.2% penetration and has held the number two position across all three waves, confirming that Spain’s public broadcaster has successfully extended its brand and catalogue into the streaming era.

→ Atresplayer (33.8%) remains a significant force with 17 million registered users and 20 million hours of video consumed monthly, even as its penetration has drifted slightly downward since Wave 1.

→ Mediaset Infinity (16.8%) had the most interesting Wave 2 story, jumping 3.8% from October to December in 2025. The start to 2026 was more challenging for the platform as it dropped 1.1%, but that is still a net +2.7%, higher than any other platform.

The international pure players:

→ YouTube dominates the Free Streaming market although YouTube’s performance fluctuates on a quarterly basis. From October to December of 2025, YouTube dropped 2.3% to 68.8%. But by February of 2026, YouTube was back up at 71.2%. It’s too soon to tell if YouTube hit a ceiling or growth is slowing down.

→ Pluto TV has become the third-largest free platform in Spain at 37.8%, gaining 2.3% in Wave 3 and now sits firmly above Atresplayer in the rankings. With 22.7% of respondents watching DAZN, it stands leaps and bounds above other sports-exclusive platforms LaLiga Sports and FIFA+. It is impressive because sports and sport content still perform well on linear television, making grabbing attention for sports content all the more competitive. DAZN had a rough December to February period, however, dropping -4.2% from its 26.9% penetration in December. Rakuten TV (19.8%) and Twitch (16.6%) round out a second tier of international platforms.

The CTV and device manufacturers: Samsung TV Plus recorded the largest point gain of any platform in Wave 3, jumping 5.2% to 22.4%, making it the biggest mover in the entire field over that period. But because the previous period was slower (leaving Samsung at only 17.2% penetration), Samsung only saw a net +1.3%. LG Channels grabs the 11th spot, Xiaomi TV+ 14th, TCL Channel 16th and Whale TV+ 18th.

One segment sits outside the GECA data but deserves a mention.